February 2nd, or Groundhog Day, is not a random date. In fact, it is the cross-quarter day, which falls between the winter solstice and the spring equinox. This means it is right between the seasons, and a good time to think about whether it is going to be a long winter, or an early spring.

Groundhogs are not the only predictors we have relied on over the years. Before Groundhog Day started in 1887, other traditions throughout Europe occupied the same day. The Celts celebrated Imbloc—a pagan festival marking the beginning of Spring. Christians in Europe celebrated Candlemas—the blessing of candles needed for a cold season. If it was a sunny day—and the candles cast shadows like Punxsutawney Phil—it was believed another forty days of winter were on the horizon.

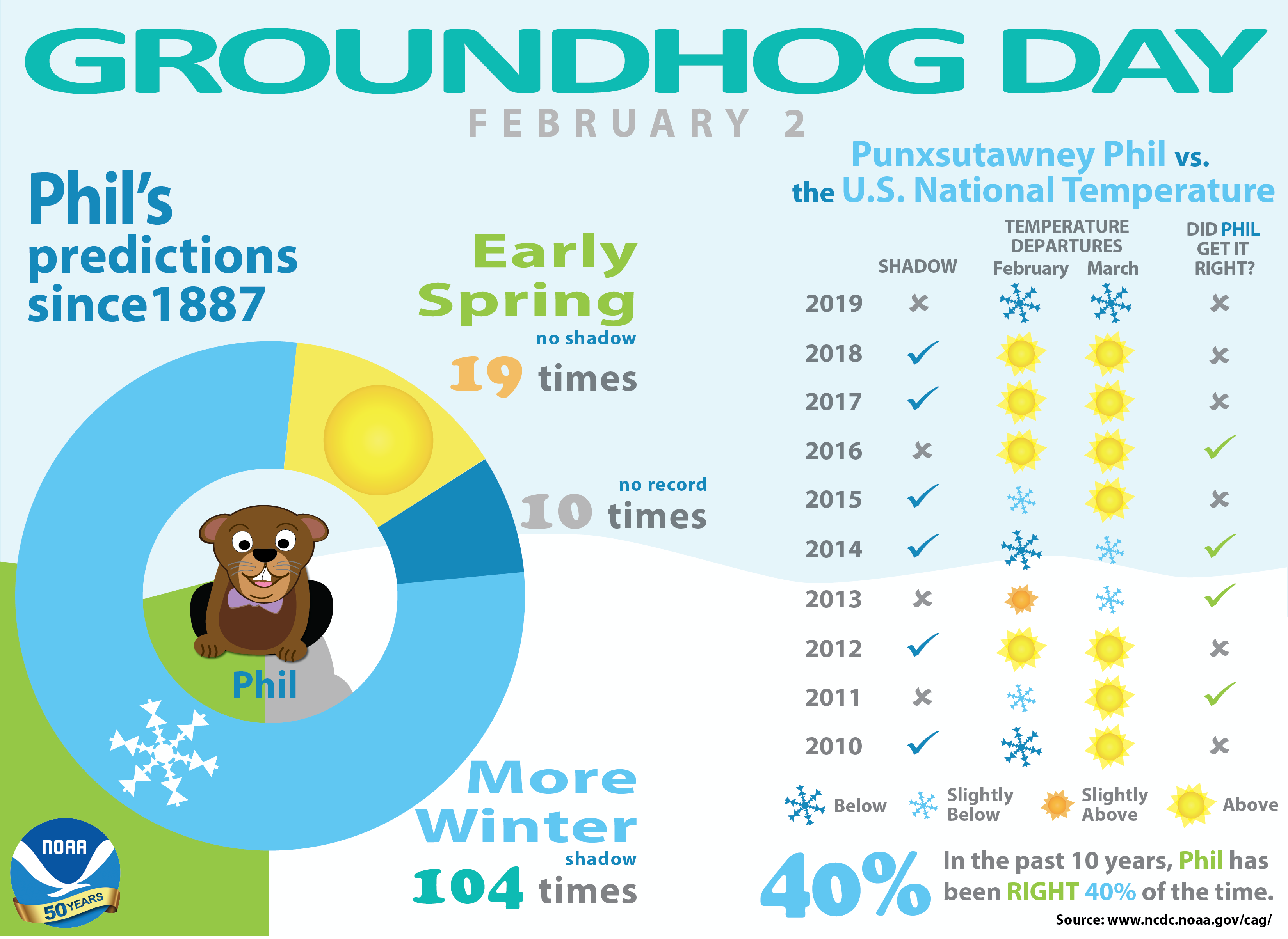

We may wish for an early spring, but its arrival has been notoriously difficult to predict. The National Centers for Environmental Information has compared Punxsutawney Phil’s forecast to actual temperatures for the 2010-2020 decade and found he has only been correct 40% of the time. Out of 125 recorded predictions, early spring was only forecast 19 times.

{kind=link}

Much as we can hope for an early spring, given the uncertainty, we’ll need to plan for both possible scenarios.

When it comes to the wealth management journey, one also creates predictions and hopes, which help motivate us and move us toward our financial goals. However, a contingency plan may bring peace of mind if those ideal plans go awry.

Predictions and Potentialities

Some predictions deal with factors outside our control, while others have actionable steps one can take to help it come to pass. At age 35, most predict life will continue until at least age 65. Additionally, many assume they will continue to financially provide for their family during those 30 years. Hopefully, it is an accurate prediction, but all kinds of accidents—some preventable, and others not—could suddenly turn that prediction on its head. On the other hand, one could purchase a 30-year term life insurance policy, thereby helping mitigate uncertainty. Suddenly the prediction about successfully financially providing for the family becomes more likely—and adding disability insurance makes the prediction even more likely.

Creating a plan B

Utilizing financial planning strategies may help families create financial stability, to respond to unforeseen circumstances. While we may be unable to predict difficult times, sound planning may allow flexible responses as events unfold. To increase financial security for your family, one could consider:

- Creating an emergency fund

- Selecting more insurance (life, long-term care, or disability insurance)

- Making portfolio changes to reduce investment risk

- Saving more in tax-preferred retirement accounts to help avoid running out money

Life events to watch for

Robust financial plans need to be dynamic and flexible. There are many life events capable of upending a financial plan, including:

- marriages

- divorces

- births

- deaths

- career changes

- personal residence changes

- economic and financial market volatility

One more we must consider due to our recent shared experience—the onset of a pandemic. The exact impact of any of these events on a family’s financial security is unpredictable. However, the impact may be substantial.

How can Arvest Help?

Client advisors, such as those at Arvest Wealth Management, can review your situation and suggest available financial options. Some strategies may be more appropriate than others depending on your family dynamic and dependents. The advisor can help with other risk-mitigation strategies by:

- Reviewing your cashflow needs and advising on liquidity of investments for “just in case” scenarios, and whether tax-deferred, less-liquid investment accounts, such as IRAs, might be appropriate.

- Revisiting your risk tolerance, as you experience life events and your situation changes, and rebalancing your portfolio accordingly.

- Providing diversification—through asset allocation—to help mitigate some of the risks of investing.

- Helping prevent hasty decisions by providing a historical perspective, which may keep you focused on your long-term goals.

Creating a wealth plan that matches your risk profile and consistently reviewing that plan can help maintain control. Click to setup a meeting with a client advisor to learn more.

This content has been prepared by The Merrill Anderson Company and is intended as a general guideline.

© 2021 M.A. Co. All rights reserved.